Tax Planning That Works Year-Round — Not Just in April

Most financial plans address what you own. Fewer address what you keep. For families building wealth in Southlake and across DFW, the gap between a good investment portfolio and a tax-efficient one often comes down to strategy — specifically, how proactively your advisor is working to reduce the taxes you pay on the growth you've earned.

Why Tax Planning Belongs at the Center of Your Financial Plan

Tax planning financial advisor conversations in Southlake often start the same way: "My accountant handles my taxes." That's a reasonable starting point — but your CPA's job is to file accurately based on what happened. Our job is to work with your CPA throughout the year to influence what happens before it does. Those are different conversations, and both matter.

At Victory Financial Group, tax planning isn't a separate service — it's woven into every financial planning engagement we take on. Capital gains timing, Roth conversion windows, account distribution sequencing, and tax-efficient investing decisions don't exist in isolation. Each one affects the others, and all of them affect your long-term outcome.

Asset Location: The Tax Strategy Most Advisors Skip

Here's a distinction that changes how you think about your portfolio: asset allocation is what you own — your mix of stocks, bonds, and other holdings. Asset location is where you hold each of those assets across your taxable, tax-deferred, and Roth accounts. Same portfolio. Potentially very different tax outcomes.

The logic is straightforward. Investments that generate ordinary income — bond interest, for example — tend to create a higher tax drag when held in a taxable brokerage account. Investments with long-term growth potential and favorable capital gains treatment may be better suited to taxable accounts where that treatment applies. Tax-inefficient assets belong in tax-deferred or Roth accounts where that drag is eliminated or deferred.

Most advisors manage allocation. Fewer manage location with the same deliberateness. We treat both as active responsibilities — and the difference compounds over time in ways that show up meaningfully in a client's retirement picture.

What Proactive Tax Planning Actually Looks Like

"Proactive" is an easy word to put on a website. Here's what it means in practice at Victory Financial Group. Tax-efficient investing in DFW requires more than selecting low-turnover funds — it requires a strategy that's revisited as your income, account balances, and tax law all shift.

Contact Us Today

Victory Financial Southlake is an independent member of the Victory Financial Group network. Rodney Tracer and Daniel Paschke are senior advisors with a combined two decades of experience serving families and business owners across the DFW area. To learn more about our approach, visit our contact page.

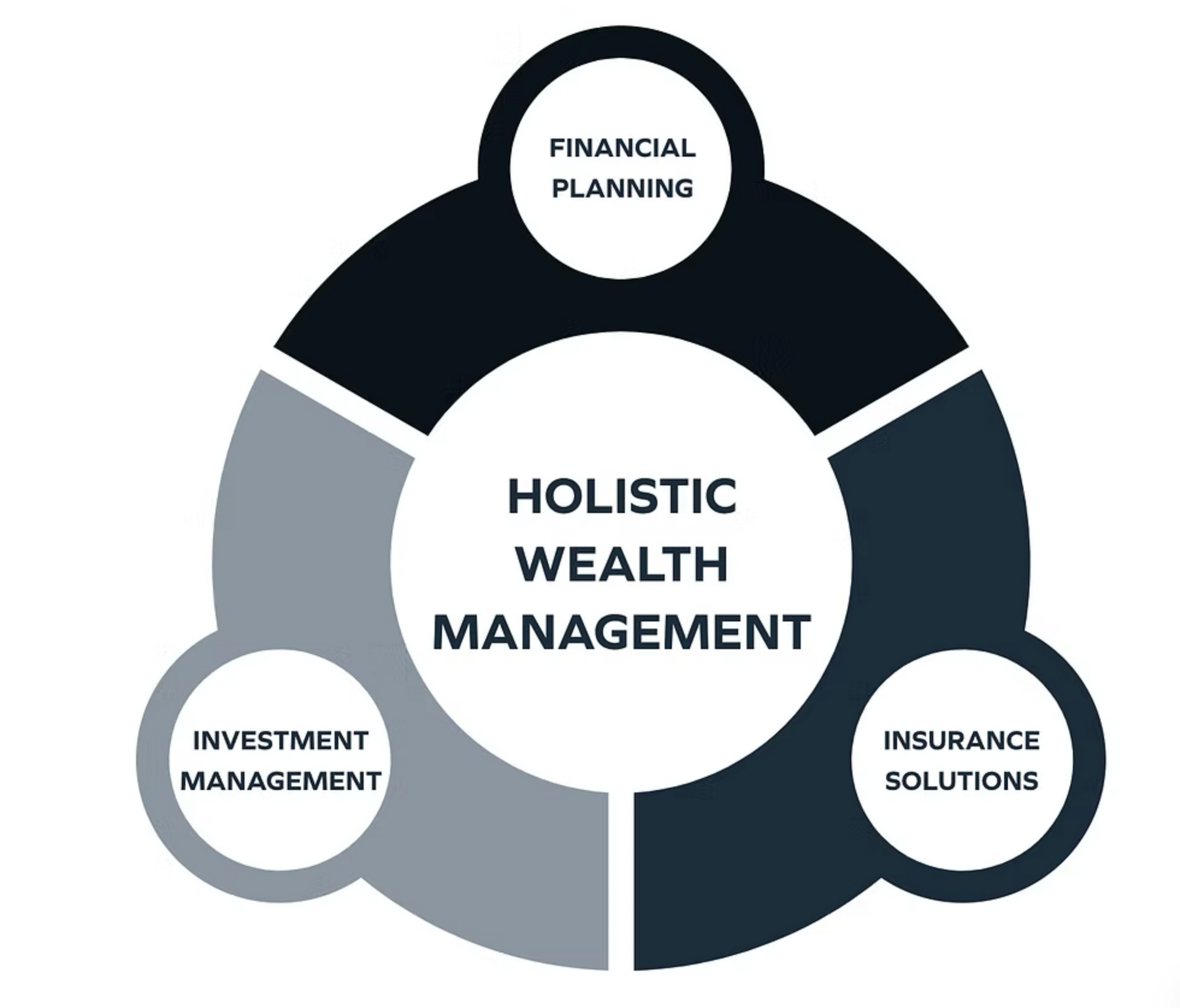

The Victory Financial Strategy

The Tax Strategies We Work Through With Clients

Each of the following represents a real planning lever — something we evaluate for every client based on their current situation, not a checklist we run through once and file away.

Roth Conversion Planning

For many pre-retirees, the years between retirement and required minimum distributions represent a narrow window of lower taxable income. A well-timed Roth conversion strategy can move money from a tax-deferred account into a Roth at a lower rate than you'd pay later — reducing your future RMD burden and creating a tax-free income source in retirement. We model conversion scenarios annually and revisit them when your income picture changes.

Capital Gains Management

Capital gains management in Texas is particularly relevant for clients with concentrated positions, appreciated real estate, or significant taxable investment accounts. We work to time gains and losses deliberately — harvesting losses when available, deferring gains when it makes sense, and coordinating with your tax professional so no decision is made in a silo.

Required Minimum Distribution Sequencing

For clients approaching or already in retirement, the order in which you draw from different account types has real tax consequences. We plan distribution sequencing as part of your overall retirement income strategy — coordinating with your estate plan and Social Security timing to keep your effective tax rate as low as possible across your retirement years.

Tax-Loss Harvesting

When markets create temporary losses in taxable accounts, those losses can be used to offset gains elsewhere in your portfolio — reducing your current-year tax liability without altering your long-term investment strategy in any meaningful way. We monitor for harvesting opportunities throughout the year, not just at year-end.

CPA and Attorney Coordination

We don't replace your accountant or estate attorney — we work alongside them. Our role is to bring the investment and planning context that your CPA may not have visibility into, and to flag planning opportunities before they become missed deadlines. Many of our clients find that having their advisor and their CPA in regular communication eliminates the gaps where tax mistakes tend to happen.

Tax Reduction Strategies in Tarrant County: What the Numbers Say

Texas has no state income tax — a meaningful advantage for wealth accumulation and retirement income planning that draws families from higher-tax states every year. But federal tax exposure doesn't disappear at the state line. For clients in Southlake, Grapevine, Trophy Club, and the broader Tarrant County area, the planning opportunity is to make full use of the Texas advantage while actively managing federal tax drag through the strategies above.

According to Vanguard research, the combination of tax-efficient fund placement and ongoing tax-loss harvesting can add meaningful value to a portfolio over time — with estimates of up to 0.70% in annual after-tax return improvement from tax-efficient investing practices alone. For a $2 million portfolio, that difference is not academic.

Frequently Asked Questions

Frequently Asked Questions About Tax Planning

What's the difference between a financial advisor and a CPA when it comes to tax planning?

A CPA's primary role is accurate tax preparation and compliance — filing based on what happened in the prior year. A financial advisor focused on tax planning works throughout the year to structure decisions before they're made: timing income, managing account withdrawals, and positioning your portfolio to reduce future tax liability. The two roles complement each other, and we coordinate actively with our clients' CPAs rather than working around them.Is Texas a good state for retirement taxes?

Texas is one of the most tax-friendly states for retirees in the country. There is no state income tax, which means Social Security, pension income, IRA distributions, and investment income are all free from state-level taxation. Property taxes in North Texas can run higher than the national average, but for most affluent retirees, the absence of a state income tax represents a significant long-term advantage — one worth factoring into both where you retire and how you structure your income.What is asset location, and why does it matter?

Asset location is the practice of placing different investments in the account types — taxable, tax-deferred, or Roth — where they'll generate the least tax drag over time. It's distinct from asset allocation, which is about what you own. Two clients with identical portfolios can have meaningfully different after-tax outcomes depending on where each holding sits. For clients with multiple account types, asset location is one of the highest-value planning decisions we make together.How often does Victory Financial Group review tax planning with clients?

Tax planning at our firm is a year-round conversation, not an annual event. We revisit tax strategy when income changes, when markets create harvesting opportunities, when tax law shifts, and as clients approach key milestones like retirement or a Roth conversion window. We also stay in contact with clients' CPAs throughout the year so that planning decisions are made with full context on both sides.Can you help with tax planning around a business sale or large capital event?

Yes. Significant capital events — business sales, concentrated stock positions, large inheritances, or real estate transactions — require careful planning in advance of the transaction, not after. We work with clients to model the tax consequences of different timing and structuring approaches and coordinate with their legal and tax counsel to pursue the most favorable outcome. If you have a capital event on the horizon, the earlier we're involved, the more options are available.