Insurance Review With No Sales Agenda — Just the Coverage Your Plan Actually Needs

Your financial plan is only as strong as the risks it accounts for. We review your insurance coverage as a formal part of your comprehensive financial plan — objectively, without commission pressure — so your protection aligns with where you are in life today, not where you were when you first bought a policy.

Why Insurance Review Belongs Inside Your Financial Plan

Most people review their insurance only when a renewal notice arrives or a salesperson calls. That's reactive planning, and it often leads to coverage that no longer fits. As a fiduciary financial advisor serving families in Southlake and across the DFW mid-cities corridor, we approach insurance planning the way it should be approached: as a risk management question embedded in your overall financial picture, not as a product transaction.

When we review your coverage, we're asking whether your current policies support your income, your family's needs, your tax strategy, and your retirement timeline — all at once. That's a different question than whether you have enough of a particular product.

What an Objective Coverage Review Looks Like

Our insurance review process is built into the onboarding experience and revisited at every annual plan review. We're not licensed to sell you a policy, and that's the point. Our role is to analyze what you have, identify gaps or redundancies, and give you a clear picture of where your coverage stands relative to your financial plan.

We work with life insurance, disability insurance, and long-term care planning for pre-retirees. For property and casualty coverage — home, auto, umbrella — we coordinate with Victory Insurance, a trusted partner in our network, who can review those policies with the same objective lens.

What we look at in a coverage review:

- Life insurance — term vs. permanent, death benefit adequacy, policy performance, and whether existing coverage still reflects your current assets and obligations

- Disability insurance — income replacement coverage for working professionals, policy definitions, and benefit period alignment with your financial plan

- Long-term care planning — funding strategies, policy structures, and the role of long-term care coverage within your broader retirement income plan

- Insurance coordination — ensuring your coverage layers work together and don't leave gaps at the intersections

The Coverage Questions We Hear Most Often

Affluent families in Southlake and the surrounding communities often come to us not because they have no insurance, but because they're not sure whether what they have still makes sense. Life changes — income grows, assets accumulate, children become independent, businesses are sold — and coverage that made sense a decade ago may be misaligned today.

These are the three areas where we most commonly find gaps or mismatches in the families we work with.

Contact Us Today

Victory Financial Southlake is an independent member of the Victory Financial Group network. Rodney Tracer and Daniel Paschke are senior advisors with a combined two decades of experience serving families and business owners across the DFW area. To learn more about our approach, visit our contact page.

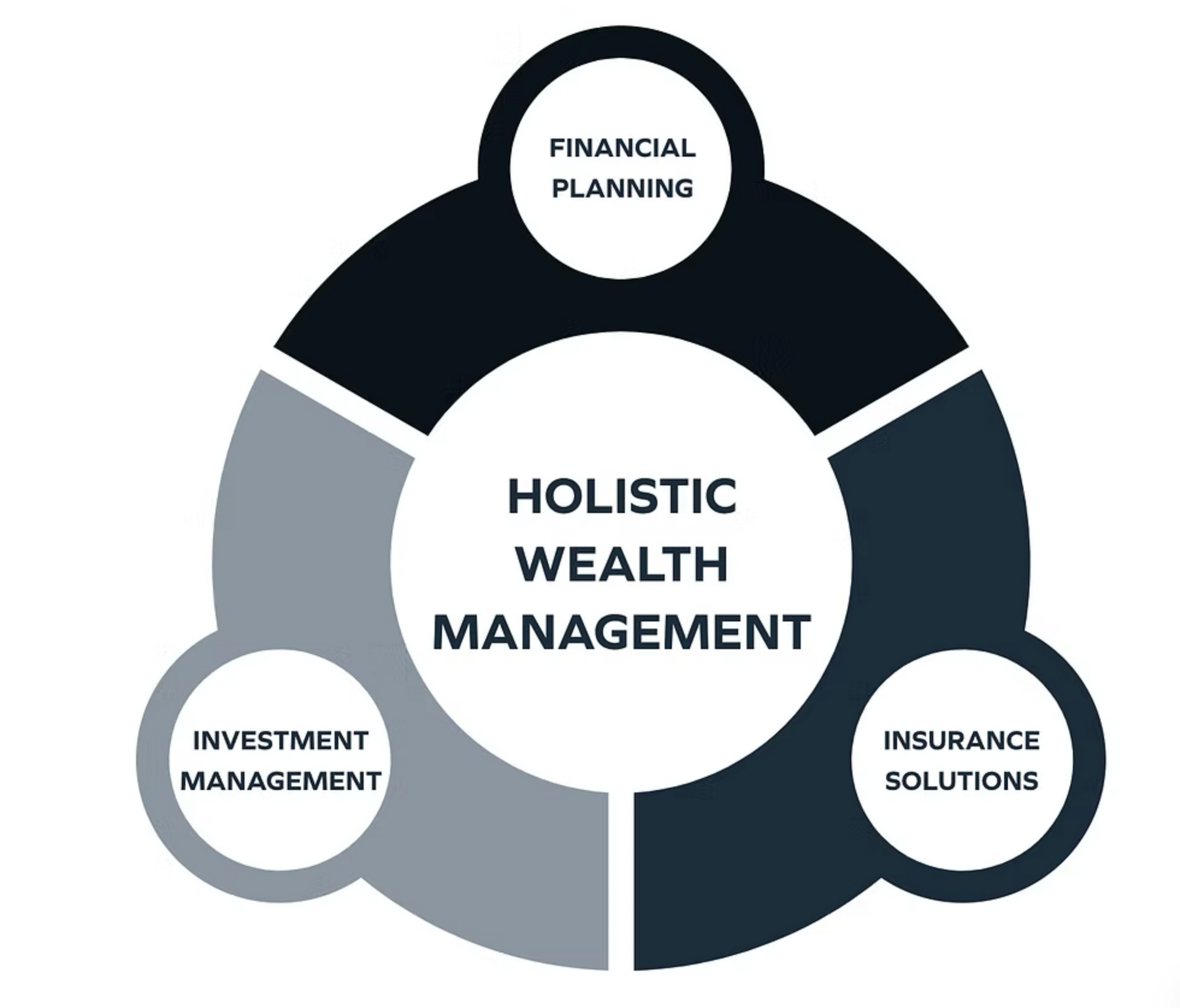

The Victory Financial Strategy

Life, Disability, and Long-Term Care — Covered in Context

Life Insurance Review for Changing Financial Lives

The question isn't just whether you have life insurance. It's whether the type, amount, and structure of your coverage still reflects your income, your debts, your estate plan, and your family's actual financial exposure. We review permanent and term policies as part of the comprehensive planning process — looking at whether a policy is performing as expected, whether the death benefit is still appropriate, and whether the structure aligns with your current tax and estate strategy.

Disability Insurance for Working Professionals

Your ability to earn income is one of the most significant financial assets you carry into retirement. Disability insurance planning for Texas professionals involves more than checking a box — it means understanding policy definitions, own-occupation provisions, benefit periods, and how disability coverage interacts with your savings rate and retirement timeline. We include this review in your financial plan so that a health event doesn't derail the trajectory you've built.

Long-Term Care Planning for Pre-Retirees

Long-term care is one of the most underplanned risks in retirement, and one of the most consequential. The cost of extended care can erode decades of savings in a short period. We work with pre-retirees in Southlake and across Tarrant County to evaluate long-term care funding strategies — whether that's a traditional policy, a hybrid life/LTC product, or a self-funding approach built into the retirement income plan — and we do it within the context of your full financial picture.

Annual Insurance Checkpoints Built Into Your Plan

Your coverage shouldn't be static. We include an insurance checkpoint in every annual plan review — updating our analysis as your income changes, your assets grow, your family situation evolves, and your retirement horizon shortens. This is what it means to plan comprehensively: the work doesn't stop at the initial review.

Property and Casualty Coordination Through Victory Insurance

For home, auto, umbrella, and other property and casualty coverage, we coordinate with Victory Insurance — a partner in our network — to ensure those policies are reviewed with the same attention to alignment and value. We make the introduction, share relevant context from your financial plan, and stay in the loop. It's one more area where we work to make sure nothing falls through the cracks.

Independent Insurance Planning in Southlake and DFW

As an independent RIA, we hold no contracts with insurance carriers and receive no commissions on insurance products. That independence is meaningful. When we tell you a policy is appropriate, it's because it fits your plan — not because it fits a sales quota. When we tell you that you may be over-insured, or that a policy is underperforming, that's an honest assessment you're unlikely to get from someone whose compensation depends on keeping the policy in force.

This is what independent insurance planning looks like when it's done inside a comprehensive financial planning relationship. Our clients in Southlake, Grapevine, Trophy Club, Westlake, and Colleyville come to us because they want advice they can trust — and that trust extends to every corner of their financial life, including coverage.

Frequently Asked Questions

Common Questions About Insurance Planning

When should I review my life insurance policy?

A life insurance review makes sense any time your financial situation changes significantly — a major income increase, a business sale, a change in marital status, children leaving the household, or a shift in your estate plan. As a general rule, reviewing your coverage every two to three years is reasonable, and we include an insurance checkpoint in every annual plan review for clients we work with on an ongoing basis.What's the difference between term and permanent life insurance, and how do I know which is right for me?

Term insurance provides a death benefit for a defined period and is typically lower cost. Permanent insurance — whole life, universal life, and indexed universal life, among others — builds cash value and lasts for your lifetime, but carries higher premiums and more complexity. The right structure depends on your income, your estate planning goals, your tax situation, and how insurance fits into your broader financial plan. We review both types objectively and without a preference for either.Do I need disability insurance if I already have coverage through my employer?

Group disability coverage through an employer is often a starting point, not a complete solution. Group policies typically replace 60% of base salary, may exclude bonuses and commissions, and are often taxable at the benefit stage. For high-income professionals in the DFW area, a personal disability policy can fill the gap between what group coverage provides and what you'd actually need to maintain your financial plan if you couldn't work.How does long-term care planning fit into a retirement income strategy?

Long-term care costs are one of the largest unplanned expenses in retirement, and they can arrive quickly. A long-term care funding strategy — whether through a standalone policy, a hybrid product, or a dedicated self-funding reserve — needs to be sized against your income sources, your assets, and your family's capacity to provide informal care. We build this analysis into the retirement planning conversation rather than treating it as a separate product decision.Does Victory Financial Group sell insurance products?

We do not sell insurance products and receive no commissions on coverage. Our role is to review your existing policies, identify gaps or misalignments, and give you an objective analysis of where your coverage stands relative to your financial plan. If you need new coverage, we can refer you to carriers or, for property and casualty needs, coordinate with Victory Insurance, a partner in our network.