A Retirement Plan Built to Last as Long as You Do

Retirement planning in Southlake means something specific — a high-cost-of-living community where the lifestyle you've built takes real income to sustain. We help pre-retirees across the DFW mid-cities corridor build retirement income plans that account for what life actually costs here, not a national average.

Know Your Number. Own Your Timeline.

The most common fear we hear from pre-retirees isn't about the market — it's about uncertainty. "Am I actually ready? What if I retire too early and run out?" We start every retirement planning engagement with a clarity conversation: mapping your current assets, projected income needs, and target timeline so you know your real retirement number, not a generic estimate built for someone else's life.

That number becomes the foundation for every decision that follows.

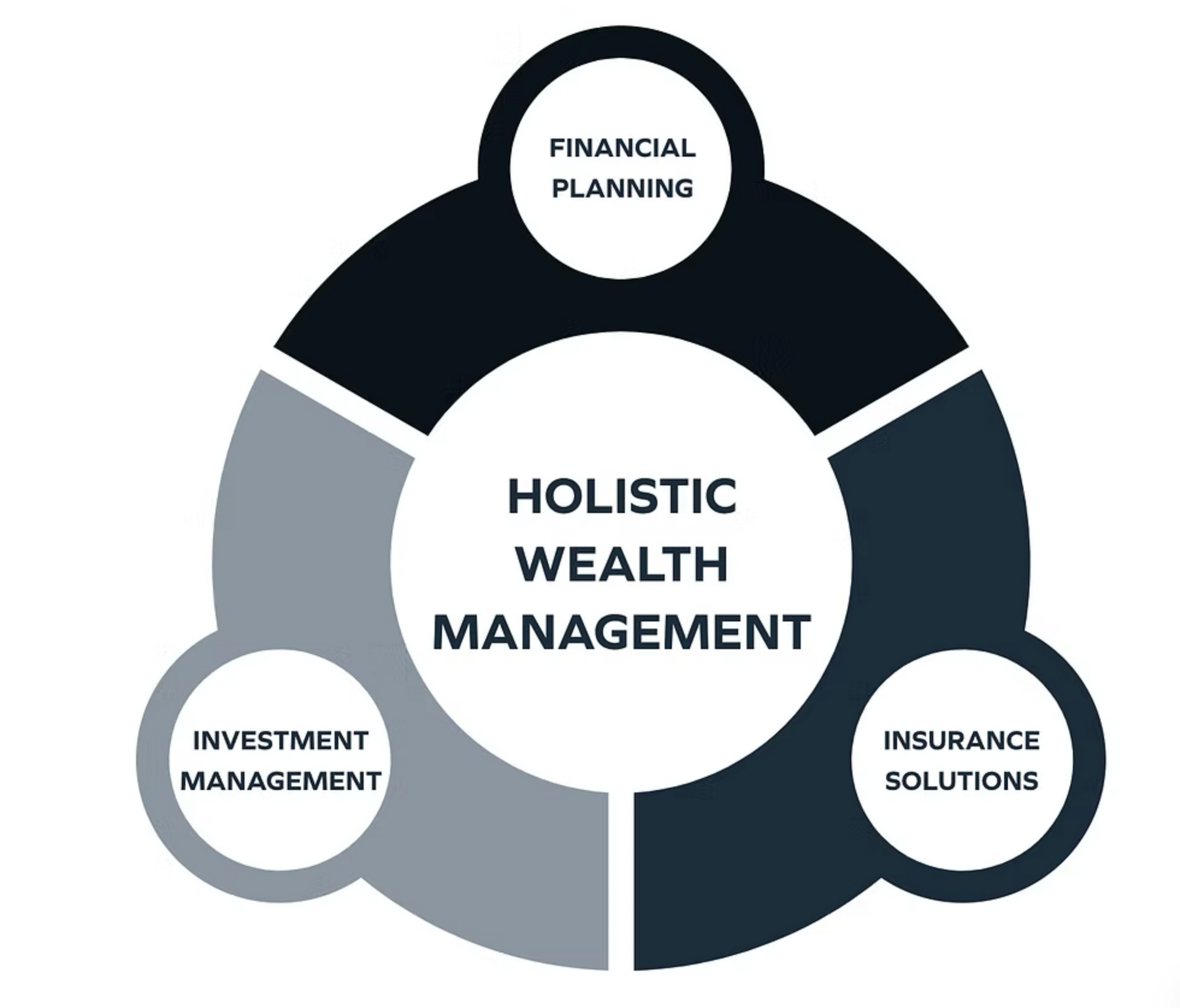

What Retirement Income Planning at Victory Financial Covers

Retirement income planning isn't a single decision — it's a coordinated sequence of decisions that have to work together. Here's what we address:

- Social Security timing strategy — maximizing your lifetime benefit based on your health, income needs, and spousal situation

- 401(k) and IRA distribution sequencing — drawing from accounts in the right order to reduce taxes and extend portfolio longevity

- Roth conversion analysis — identifying the right windows to convert pre-tax assets before RMDs begin

- Required Minimum Distribution planning — managing RMD impact on your tax bracket and Medicare premiums

- Portfolio longevity modeling — stress-testing your income plan across market cycles and longer-than-expected retirements

- Insurance and income gap review — evaluating whether long-term care, annuities, or other income sources belong in your plan

Income for Life — Not Just for Now

The sequence in which you draw from your accounts matters as much as how much you've saved. Drawing from the wrong account at the wrong time can accelerate your tax burden, trigger higher Medicare premiums, or shrink the assets you intended to leave behind. We build distribution strategies that coordinate your taxable, tax-deferred, and tax-free accounts — so your income is sustainable, your tax exposure is managed, and your plan holds up across decades, not just the first few years of retirement.

This is where tax planning and retirement planning converge, and it's one of the areas where working with a comprehensive planning firm makes the most measurable difference.

Contact Us Today

Victory Financial Southlake is an independent member of the Victory Financial Group network. Rodney Tracer and Daniel Paschke are senior advisors with a combined two decades of experience serving families and business owners across the DFW area. To learn more about our approach, visit our contact page.

The Victory Financial Strategy

Our Retirement Planning Process

We follow a structured 12–18 month onboarding roadmap that moves from discovery through full implementation — so nothing falls through the cracks and every piece of your plan connects.

1. Clarity Conversation

We map your current financial picture: assets, income sources, expected expenses, and retirement timeline. The goal is to define your actual retirement number and identify any gaps between where you are and where you need to be.

2. Income Architecture

We model your distribution strategy — sequencing withdrawals across account types, timing Social Security, and running Roth conversion scenarios to minimize your lifetime tax burden.

3. Portfolio Alignment

We review your investment allocation through the lens of retirement income, not just growth. That means evaluating risk, liquidity, and asset location — which assets belong in which accounts to reduce drag and improve after-tax returns.

4. Full Plan Delivery

You receive a written retirement income plan with a clear timeline, decision points, and implementation steps. We walk through it together so you understand every recommendation before anything is executed.

5. Ongoing Review

Retirement planning isn't a one-time event. We meet regularly to revisit your plan as tax law, market conditions, and your life circumstances change.

What Retirement Really Looks Like in Southlake

For many of our clients, retirement in Southlake means staying close to the community they've built — spending more time at Town Square, traveling through DFW and beyond, staying active on the lake, and being present for family nearby. That lifestyle has a real cost, and your retirement income plan should reflect it.

We work with clients who have accumulated meaningful wealth and want to make sure it's structured to support the life they've earned — not just to clear a generic retirement benchmark.

Frequently Asked Questions

Frequently Asked Questions About Retirement Planning

When should I start retirement planning in Southlake?

The most productive retirement planning typically happens in the 5–10 years before your target retirement date — what's often called the "retirement red zone." This is the window where Roth conversion opportunities are most valuable, Social Security strategy decisions carry the most weight, and distribution sequencing can meaningfully reduce your lifetime tax burden. That said, we work with clients at all stages, and earlier planning almost always creates more options.How do I figure out when I can actually retire?

It starts with understanding your income gap — the difference between what your assets and guaranteed income sources (Social Security, pensions, rental income) will produce and what your retirement lifestyle will actually cost. We model this specifically for your situation, accounting for Southlake's cost of living, your expected healthcare costs, and a realistic retirement timeline. The goal is a clear answer, not a range.What's the best strategy for Social Security timing?

There's no universal right answer — the optimal timing depends on your health, your spouse's benefit, your other income sources, and your tax situation. For many of our clients, delaying Social Security while drawing from other accounts first produces a meaningfully higher lifetime benefit. We run the analysis as part of every retirement income plan.How does a Roth conversion fit into retirement planning?

Roth conversions are most valuable in the years between retirement and age 73, when your income may be lower and before Required Minimum Distributions begin. Converting pre-tax assets to Roth during this window can reduce future RMDs, lower your lifetime tax burden, and create tax-free income later. Whether a conversion makes sense — and how much to convert each year — depends on your current bracket, projected future income, and estate goals.What makes Victory Financial Group different from other retirement planners in DFW?

We're a fiduciary, independent RIA — which means we're not selling products and we're not tied to any proprietary investment platform. All three of our advisors grew up in this community, which means we understand the financial profile and lifestyle priorities of Southlake and NE Tarrant County clients. And because we handle comprehensive planning — investments, tax strategy, estate planning, and insurance — your retirement plan connects to every other part of your financial life rather than existing in isolation.